Although blockchain is a new technology, it already boasts a rich and

interesting history. The following is a brief timeline of some of the most

important and notable events in the development of blockchain.

Satoshi Nakamoto, a pseudonym for a person or group, publishes “Bitcoin: A Peer to Peer Electronic Cash System."

The first successful Bitcoin (BTC) transaction occurs between computer scientist Hal Finney and the mysterious Satoshi Nakamoto.

Florida-based programmer Laszlo Hanycez completes the first-ever purchase using Bitcoin — two Papa John’s pizzas. Hanycez transferred 10,000 BTC’s, worth about $60 at the time. Today it's worth $80 million.

The market cap of Bitcoin officially exceeds $1 million.

1 BTC = $1USD, giving the cryptocurrency parity with the US dollar.

Electronic Frontier Foundation, Wikileaks and other organizations start accepting Bitcoin as donations.

Blockchain and cryptocurrency are mentioned in popular television shows like The Good Wife, injecting blockchain into pop culture.

Bitcoin Magazine launched by early Bitcoin developer Vitalik Buterin.

BTC market cap surpassed $1 billion.

Bitcoin reached $100/BTC for the first time.

Buterin publishes “Ethereum Project" paper suggesting that blockchain has other possibilities besides Bitcoin (e.g., smart contracts).

Gaming company Zynga, The D Las Vegas Hotel and Overstock.com all start accepting Bitcoin as payment.

Buterin’s Ethereum Project is crowdfunded via an Initial Coin Offering (ICO) raising over $18 million in BTC and opening up new avenues for blockchain.

R3, a group of over 200 blockchain firms, is formed to discover new ways blockchain can be implemented in technology.

PayPal announces Bitcoin integration.

Filecoin

Filecoin is an open-source cloud storage marketplace, protocol, and cryptocurrency.

What Is a Hard Fork?

A hard fork (or hardfork), as it relates to blockchain technology, is a radical change to a network's protocol that makes previously invalid blocks and transactions valid, or vice-versa. A hard fork requires all nodes or users to upgrade to the latest version of the protocol software.

Forks may be initiated by developers or members of a crypto community who grow dissatisfied with functionalities offered by existing blockchain implementations. They may also emerge as a way to crowdsource funding for new technology projects or cryptocurrency offerings.

A hard fork refers to a radical change to the protocol of a blockchain network that effectively results in two branches, one that follows the previous protocol and one that follows the new version.

In a hard fork, holders of tokens in the original blockchain will be granted tokens in the new fork as well, but miners must choose which blockchain to continue verifying.

A hard fork can occur in any blockchain, and not only Bitcoin (where hard forks have created Bitcoin Cash and Bitcoin SV, among several others, for example).

A fork in a blockchain can occur in any crypto-technology platform—not only Bitcoin. That is because blockchains and cryptocurrency work in basically the same way no matter which crypto platform they're on. You may think of the blocks in blockchains as cryptographic keys that move memory. Because the miners in a blockchain set the rules that move the memory in the network, these miners understand the new rules.

However, all of the miners need to agree about the new rules and about what comprises a valid block in the chain. So when you want to change those rules you need to "fork it"—like a fork in a road—to indicate that there's been a change in or a diversion to the protocol. The developers can then update all of the software to reflect the new rules.

It is through this forking process that various digital currencies with names similar to bitcoin have come to be: bitcoin cash, bitcoin gold, and others. For the casual cryptocurrency investor, it can be difficult to tell the difference between these cryptocurrencies and to map the various forks onto a timeline.

Understanding Bitcoin Hard Forks

In 2009, shortly after releasing bitcoin, Satoshi mined the first block on the bitcoin blockchain.

This has come to be referred to as the Genesis Block, as it represented the founding of the cryptocurrency as we know it. Satoshi was able to make numerous changes to the bitcoin network early on in this process; this has become increasingly difficult and bitcoin's user base has grown by a tremendous margin.

The fact that no one person or group can determine when and how bitcoin should be upgraded has similarly made the process of updating the system more complex. In the years following the Genesis Block, there have been several hard forks.

In addition to hard forks, cryptocurrencies, including bitcoin, also undergo soft forks. The difference between a hard fork and a soft fork is that soft forks do not result in a new currency. Soft forks are a change to the bitcoin protocol, but the end product remains unchanged. Soft forks are backward compatible.

During a hard fork, software implementing bitcoin and its mining procedures is upgraded; once a user upgrades their software, that version rejects all transactions from older software, effectively creating a new branch of the blockchain. However, those users who retain the old software continue to process transactions, meaning that there is a parallel set of transactions taking place across two different chains.

Bitcoin XT

Bitcoin XT was one of the first notable hard forks of bitcoin. The software was launched by Mike Hearn in late 2014 in order to include several new features he had proposed. While the previous version of bitcoin allowed up to seven transactions per second, Bitcoin XT aimed for 24 transactions per second. In order to accomplish this, it proposed increasing the block size from one megabyte to eight megabytes. Bitcoin XT initially saw success, with more than 1,000 nodes running its software in the late summer of 2015.

However, just a few months later, the project lost user interest and was essentially abandoned by its users. Bitcoin XT is no longer available, with its original website now defunct.

Bitcoin Classic

When Bitcoin XT declined, some community members still wanted block sizes to increase. In response, a group of developers launched Bitcoin Classic in early 2016. Unlike XT, which proposed increasing the block size to eight megabytes, classic intended to increase it to only two megabytes.

Like Bitcoin XT, Bitcoin Classic saw initial interest, with about 2,000 nodes for several months during 2016. The project also still exists today, with some developers strongly supporting Bitcoin Classic. Nonetheless, the larger cryptocurrency community seems to have generally moved on to other options.

Bitcoin Unlimited

Bitcoin Unlimited has remained something of an enigma since its release in early 2016. The project's developers released code but did not specify which type of fork it would require. Bitcoin Unlimited set itself apart by allowing miners to decide on the size of their blocks, with nodes and miners limiting the size of blocks they accept, up to 16 megabytes.

Despite some lingering interest, bitcoin unlimited has largely failed to gain acceptance.

Segregated Witness

Bitcoin Core developer Pieter Wuille presented the idea of Segregated Witness (SegWit) in late 2015. Put simply, SegWit aims to reduce the size of each bitcoin transaction, thereby allowing more transactions to take place at once. SegWit was technically a soft fork. However, it may have helped to prompt hard forks after it was originally proposed.

Trading Cryptocurrencies

How Does Trading Cryptocurrencies Differ from Stocks?

While you can invest in cryptocurrencies, they differ a great deal from traditional investments, like stocks. When you buy stock, you are buying a share of ownership of a company, which means you’re entitled to do things like vote on the direction of the company. If that company goes bankrupt, you also may receive some compensation once its creditors have been paid from its liquidated assets.

Buying cryptocurrency doesn’t grant you ownership over anything except the token itself; it’s more like exchanging one form of currency for another. If the crypto loses its value, you won’t receive anything after the fact.

There are several other key differences to keep in mind:

Trading hours: Stocks are only traded during stock exchange hours, typically 9:30 am to 4:30 pm ET, Monday through Friday. Cryptocurrency markets never close, so you can trade 24 hours a day, seven days a week.

Regulation: Stocks are regulated financial products, meaning a governing body verifies their credentials and their finances are matters of public record. By contrast, cryptocurrencies are not regulated investment vehicles, so you may not be aware of the inner dynamics of your crypto or the developers working on it.

Volatility: Both stocks and cryptocurrency involve risk; the money you invest can lose value. However, stocks are directly linked to companies and generally rise and fall based on those companies’ performance. Cryptocurrency prices are more speculative—no one is quite sure of their value yet. That makes them much more volatile and affected by something as small as a celebrity’s tweet.

Cryptocurrencies are speculative investments and should only be made if you’re willing to accept wild price swings and a decent risk of losing everything.

Cryptocurrencies:

A cryptocurrency, broadly defined, is virtual or digital money that takes the form of tokens or “coins.” While some cryptocurrencies have ventured into the physical world with credit cards or other projects, the large majority remain entirely intangible.

The “crypto” in cryptocurrencies refers to complicated cryptography that allows for the creation and processing of digital currencies and their transactions across decentralized systems. Alongside this important “crypto” feature of these currencies is a common commitment to decentralization; cryptocurrencies are typically developed as code by teams who build in mechanisms for issuance (often, although not always, through a process called “mining”) and other controls.

Cryptocurrencies are almost always designed to be free from government manipulation and control, although as they have grown more popular, this foundational aspect of the industry has come under fire. The currencies modeled after Bitcoin are collectively called altcoins, and in some cases “shitcoins,” and have often tried to present themselves as modified or improved versions of Bitcoin. While some of these currencies may have some impressive features that Bitcoin does not, matching the level of security that Bitcoin’s networks achieve largely has yet to be seen by an altcoin.

The field of cryptocurrencies has expanded dramatically since Bitcoin was launched over a decade ago, and the next great digital token may be released tomorrow.

Bitcoin continues to lead the pack of cryptocurrencies in terms of market capitalization, user base, and popularity.

Other virtual currencies such as Ethereum are being used to create decentralized financial systems for those without access to traditional financial products.

Some altcoins are being endorsed as they have newer features than Bitcoin, such as the ability to handle more transactions per second or use different consensus algorithms like proof-of-stake.

It is impossible for a list to be entirely comprehensive. One reason for this is the fact that there are more than 4,000 cryptocurrencies in existence as of January 2021. While many of these cryptos have little to no following or trading volume, some enjoy immense popularity among dedicated communities of backers and investors.

The field of cryptocurrencies is always expanding, and the next great digital token may be released tomorrow. While Bitcoin is widely seen as a pioneer in the world of cryptocurrencies, analysts adopt many approaches for evaluating tokens other than BTC. It’s common, for instance, for analysts to attribute a great deal of importance to ranking coins relative to one another in terms of market capitalization. We’ve factored this into consideration, but there are other reasons why a digital token may be included in the list as well.

The first Bitcoin alternative,- Ethereum - is a decentralized software platform that enables smart contracts and decentralized applications (dapps) to be built and run without any downtime, fraud, control, or interference from a third party. The goal behind Ethereum is to create a decentralized suite of financial products that anyone in the world can freely access, regardless of nationality, ethnicity, or faith. This aspect makes the implications for those in some countries more compelling, as those without state infrastructure and state identifications can get access to bank accounts, loans, insurance, or a variety of other financial products.

The applications on Ethereum are run on ether, its platform-specific cryptographic token. Ether is like a vehicle for moving around on the Ethereum platform and is sought mostly by developers looking to develop and run applications inside Ethereum, or now, by investors looking to make purchases of other digital currencies using ether. Ether, launched in 2015, is currently the second-largest digital currency by market capitalization after Bitcoin, although it lags behind the dominant cryptocurrency by a significant margin. As of January 2021, ether’s market cap is roughly 19% of Bitcoin’s size.

In 2014, Ethereum launched a presale for ether, which received an overwhelming response; this helped to usher in the age of the initial coin offering (ICO). According to Ethereum, it can be used to “codify, decentralize, secure and trade just about anything.” Following the attack on the decentralized autonomous organization (DAO) in 2016, Ethereum was split into Ethereum (ETH) and Ethereum Classic (ETC). As of January 2021, Ethereum (ETH) has a market capitalization of $138.3 billion and a per-token value of $1,218.59.

In 2021, Ethereum plans to change its consensus algorithm from proof-of-work to proof-of-stake. This move will allow Ethereum’s network to run itself with far less energy and improved transaction speed. Proof-of-stake allows network participants to “stake” their ether to the network. This process helps to secure the network and process the transactions that occur. Those who do this are rewarded ether, similar to an interest account. This is an alternative to Bitcoin’s proof-of-work mechanism, where miners are rewarded more Bitcoin for processing transactions.

Litecoin, - launched in 2011, was among the first cryptocurrencies to follow in the footsteps of Bitcoin and has often been referred to as “silver to Bitcoin’s gold.” It was created by Charlie Lee, an MIT graduate and former Google engineer.

Litecoin is based on an open-source global payment network that is not controlled by any central authority and uses “scrypt” as a proof of work, which can be decoded with the help of consumer-grade CPUs. Although Litecoin is like Bitcoin in many ways, it has a faster block generation rate and hence offers a faster transaction confirmation time. Other than developers, there are a growing number of merchants that accept Litecoin. As of January 2021, Litecoin has a market capitalization of $10.1 billion and a per-token value of $153.88, making it the sixth-largest cryptocurrency in the world.

Cardano - is an “Ouroboros proof-of-stake” cryptocurrency that was created with a research-based approach by engineers, mathematicians, and cryptography experts. The project was cofounded by Charles Hoskinson, one of the five initial founding members of Ethereum. After having some disagreements with the direction Ethereum was taking, he left and later helped to create Cardano.

The team behind Cardano created its blockchain through extensive experimentation and peer-reviewed research. The researchers behind the project have written over 90 papers on blockchain technology across a range of topics. This research is the backbone of Cardano.

Due to this rigorous process, Cardano seems to stand out among its proof-of-stake peers as well as other large cryptocurrencies. Cardano has also been dubbed the “Ethereum killer,” as its blockchain is said to be capable of more. That said, Cardano is still in its early stages. While it has beaten Ethereum to the proof-of-stake consensus model, it still has a long way to go in terms of decentralized financial applications.

Cardano aims to be the world’s financial operating system by establishing decentralized financial products similar to Ethereum as well as providing solutions for chain interoperability, voter fraud, and legal contract tracing, among other things. As of January 2021, Cardano has a market capitalization of $9.8 billion and one ADA trades for $0.31.

Polkadot - is a unique proof-of-stake cryptocurrency that is aimed at delivering interoperability among other blockchains. Its protocol is designed to connect permissioned and permission-less blockchains, as well as oracles, to allow systems to work together under one roof.

Polkadot’s core component is its relay chain that allows the interoperability of varying networks. It also allows for “parachains,” or parallel blockchains with their own native tokens for specific-use cases.

Where Polkadot differs from Ethereum is that rather than creating just decentralized applications on Polkadot, developers can create their own blockchain while also using the security that Polkadot’s chain already has. With Ethereum, developers can create new blockchains but need to create their own security measures, which can leave new and smaller projects open to attack, as the larger a blockchain, the more security it has. This concept in Polkadot is known as shared security.

Polkadot was created by Gavin Wood, another member of the core founders of the Ethereum project who had differing opinions on the project’s future. As of January 2021, Polkadot has a market capitalization of $11.2 billion and one DOT trades for $12.54.

Bitcoin Cash (BCH) - holds an important place in the history of altcoins because it is one of the earliest and most successful hard forks of the original Bitcoin. In the cryptocurrency world, a fork takes place as the result of debates and arguments between developers and miners. Due to the decentralized nature of digital currencies, wholesale changes to the code underlying the token or coin at hand must be made due to general consensus; the mechanism for this process varies according to the particular cryptocurrency.

When different factions can’t agree, sometimes the digital currency is split, with the original chain remaining true to its original code and the new chain beginning life as a new version of the prior coin, complete with changes to its code.

BCH began its life in August 2017 as a result of one of these splits. The debate that led to the creation of BCH had to do with the issue of scalability; the Bitcoin network has a limit on the size of blocks: one megabyte (MB). BCH increases the block size from one MB to eight MBs, with the idea being that larger blocks can hold more transactions within them, and the transaction speed would therefore be increased. It also makes other changes, including the removal of the Segregated Witness protocol that impacts block space. As of January 2021, BCH has a market capitalization of $8.9 billion and a value per token of $513.45.

Stellar - is an open blockchain network designed to provide enterprise solutions by connecting financial institutions for the purpose of large transactions. Huge transactions between banks and investment firms—typically taking several days, involving a number of intermediaries, and costing a good deal of money—can now be done nearly instantaneously with no intermediaries and cost little to nothing for those making the transaction.

While Stellar has positioned itself as an enterprise blockchain for institutional transactions, it is still an open blockchain that can be used by anyone. The system allows for cross-border transactions among any currencies. Stellar’s native currency is Lumens (XLM). The network requires users to hold Lumens to be able to transact on the network.

Stellar was founded by Jed McCaleb, a founding member of Ripple Labs and developer of the Ripple protocol. He eventually left his role with Ripple and went on to cofound the Stellar Development Foundation. Stellar Lumens have a market capitalization of $6.1 billion and are valued at $0.27 as of January 2021.

Chainlink - is a decentralized oracle network that bridges the gap between smart contracts, like the ones on Ethereum, and data outside of it. Blockchains themselves do not have the ability to connect to outside applications in a trusted manner. Chainlink’s decentralized oracles allow smart contracts to communicate with outside data so that the contracts can be executed based on data that Ethereum itself cannot connect to.

Chainlink’s blog details a number of use cases for its system. One of the many use cases that are explained would be to monitor water supplies for pollution or illegal syphoning going on in certain cities. Sensors could be set up to monitor corporate consumption, water tables, and the levels of local bodies of water. A Chainlink oracle could track this data and feed it directly into a smart contract. The smart contract could be set up to execute fines, release flood warnings to cities, or invoice companies using too much of a city’s water with the incoming data from the oracle.

Chainlink was developed by Sergey Nazarov along with Steve Ellis. As of January 2021, Chainlink’s market capitalization is $8.6 billion and one LINK is valued at $21.53.

Binance Coin - is a utility cryptocurrency that operates as a payment method for the fees associated with trading on the Binance Exchange. Those who use the token as a means of payment for the exchange can trade at a discount. Binance Coin’s blockchain is also the platform that Binance’s decentralized exchange operates on. The Binance exchange was founded by Changpeng Zhao and is one of the most widely used exchanges in the world based on trading volumes.

Binance Coin was initially an ERC-20 token that operated on the Ethereum blockchain. It eventually had its own mainnet launch. The network uses a proof-of-stake consensus model. As of January 2021, Binance has a $6.8 billion market capitalization with one BNB having a value of $44.26.

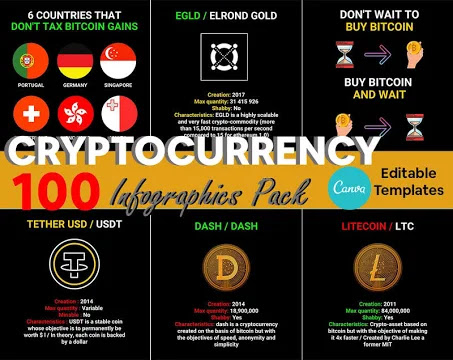

Tether {USDT} - was one of the first and most popular of a group of so-called stablecoins, cryptocurrencies that aim to peg their market value to a currency or other external reference point to reduce volatility. Because most digital currencies, even major ones like Bitcoin, have experienced frequent periods of dramatic volatility, Tether and other stablecoins attempt to smooth out price fluctuations to attract users who may otherwise be cautious. Tether’s price is tied directly to the price of the U.S. dollar. The system allows users to more easily make transfers from other cryptocurrencies back to U.S. dollars in a more timely manner than actually converting to normal currency.

Launched in 2014, Tether describes itself as “a blockchain-enabled platform designed to facilitate the use of fiat currencies in a digital manner.” Effectively, this cryptocurrency allows individuals to utilize a blockchain network and related technologies to transact in traditional currencies while minimizing the volatility and complexity often associated with digital currencies. As of January 2021, Tether is the third-largest cryptocurrency by market capitalization, with a total market cap of $24.4 billion and a per-token value of $1.

Monero - is a secure, private, and untraceable currency. This open-source cryptocurrency was launched in April 2014 and soon garnered great interest among the cryptography community and enthusiasts. The development of this cryptocurrency is completely donation-based and community-driven. Monero has been launched with a strong focus on decentralization and scalability, and it enables complete privacy by using a special technique called “ring signatures.”

With this technique, a group of cryptographic signatures appears, including at least one real participant, but the real one cannot be isolated since they all appear valid. Because of exceptional security mechanisms like this, Monero has developed something of an unsavory reputation—it has been linked to criminal operations around the world. While this is a prime candidate for making criminal transactions anonymously, the privacy inherent in Monero is also helpful to dissidents of oppressive regimes around the world. As of January 2021, Monero has a market capitalization of $2.8 billion and a per-token value of $158.37.

Blockchain technology is most simply defined as a decentralized, distributed ledger that records the provenance of a digital asset. By inherent design, the data on a blockchain is unable to be modified, which makes it a legitimate disruptor for industries like payments, cybersecurity and healthcare.

Blockchain, sometimes referred to as Distributed Ledger Technology (DLT), makes the history of any digital asset unalterable and transparent through the use of decentralization and cryptographic hashing.

A simple analogy for understanding blockchain technology is a Google Doc. When we create a document and share it with a group of people, the document is distributed instead of copied or transferred. This creates a decentralized distribution chain that gives everyone access to the document at the same time. No one is locked out awaiting changes from another party, while all modifications to the doc are being recorded in real-time, making changes completely transparent.

A blockchain is a database that stores encrypted blocks of data then chains them together to form a chronological single-source-of-truth for the data. Digital assets are distributed instead of copied or transferred, creating an immutable record of an asset. The asset is decentralized, allowing full real-time access and transparency to the public. A transparent ledger of changes preserves integrity of the document, which creates trust in the asset. Blockchain’s inherent security measures and public ledger make it a prime technology for almost every single sector.

Blockchain is an especially promising and revolutionary technology because it helps reduce risk, stamps out fraud and brings transparency in a scalable way for myriad uses.

The whole point of using a blockchain is to let people — in particular, people who don't trust one another — share valuable data in a secure, tamperproof way.

Blockchain consists of three important concepts: blocks, nodes and miners.

Every chain consists of multiple blocks and each block has three basic elements:

The data in the block.

A 32-bit whole number called a nonce. The nonce is randomly generated when a block is created, which then generates a block header hash.

The hash is a 256-bit number wedded to the nonce. It must start with a huge number of zeroes (i.e., be extremely small).

When the first block of a chain is created, a nonce generates the cryptographic hash. The data in the block is considered signed and forever tied to the nonce and hash unless it is mined.

Miners create new blocks on the chain through a process called mining.

In a blockchain every block has its own unique nonce and hash, but also references the hash of the previous block in the chain, so mining a block isn't easy, especially on large chains.

Miners use special software to solve the incredibly complex math problem of finding a nonce that generates an accepted hash. Because the nonce is only 32 bits and the hash is 256, there are roughly four billion possible nonce-hash combinations that must be mined before the right one is found. When that happens miners are said to have found the "golden nonce" and their block is added to the chain.

Making a change to any block earlier in the chain requires re-mining not just the block with the change, but all of the blocks that come after. This is why it's extremely difficult to manipulate blockchain technology. Think of it as "safety in math" since finding golden nonces requires an enormous amount of time and computing power.

When a block is successfully mined, the change is accepted by all of the nodes on the network and the miner is rewarded financially.

One of the most important concepts in blockchain technology is decentralization. No one computer or organization can own the chain. Instead, it is a distributed ledger via the nodes connected to the chain. Nodes can be any kind of electronic device that maintains copies of the blockchain and keeps the network functioning.

Every node has its own copy of the blockchain and the network must algorithmically approve any newly mined block for the chain to be updated, trusted and verified. Since blockchains are transparent, every action in the ledger can be easily checked and viewed. Each participant is given a unique alphanumeric identification number that shows their transactions.

Combining public information with a system of checks-and-balances helps the blockchain maintain integrity and creates trust among users. Essentially, blockchains can be thought of as the scalability of trust via technology.

Blockchain’s most well-known use (and maybe most controversial) is in cryptocurrencies. Cryptocurrencies are digital currencies (or tokens), like Bitcoin, Ethereum or Litecoin, that can be used to buy goods and services. Just like a digital form of cash, crypto can be used to buy everything from your lunch to your next home. Unlike cash, crypto uses blockchain to act as both a public ledger and an enhanced cryptographic security system, so online transactions are always recorded and secured.

To date, there are roughly 6,700 cryptocurrencies in the world that have a total market cap around $1.6 trillion, with Bitcoin holding a majority of the value. These tokens have become incredibly popular over the last few years, with one Bitcoin equaling $60,000. Here are some of the main reasons why everyone is suddenly taking notice of cryptocurrencies:

Blockchain’s security makes theft much harder since each cryptocurrency has its own irrefutable identifiable number that is attached to one owner.

Crypto reduces the need for individualized currencies and central banks- With blockchain, crypto can be sent to anywhere and anyone in the world without the need for currency exchanging or without interference from central banks.

Cryptocurrencies can make some people rich- Speculators have been driving up the price of crypto, especially Bitcoin, helping some early adopters to become billionaires. Whether this is actually a positive has yet to be seen, as some retractors believe that speculators do not have the long-term benefits of crypto in mind.

More and more large corporations are coming around to the idea of a blockchain-based digital currency for payments. In February 2021, Tesla famously announced that it would invest $1.5 billion into Bitcoin and accept it as payment for their cars.

Of course, there are many legitimate arguments against blockchain-based digital currencies. First, crypto isn’t a very regulated market. Many governments were quick to jump into crypto, but few have a staunch set of codified laws regarding it. Additionally, crypto is incredibly volatile due to those aforementioned speculators. In 2016, Bitcoin was priced around $450 per token. It then jumped to about $16,000 a token in 2018, dipped to around $3,100, then has since increased to more than $60,000. Lack of stability has caused some people to get very rich, while a majority have still lost thousands.

Whether or not digital currencies are the future remains to be seen. For now, it seems as if blockchain’s meteoric rise is more starting to take root in reality than pure hype. Though it’s still making headway in this entirely new, highly exploratory field, blockchain is also showing promise beyond Bitcoin.

Originally created as the ultra-transparent ledger system for Bitcoin to operate on, blockchain has long been associated with cryptocurrency, but the technology's transparency and security have seen growing adoption in a number of areas, much of which can be traced back to the development of the Ethereum blockchain.

In late 2013, Russian-Canadian developer Vitalik Buterin published a white paper that proposed a platform combining traditional blockchain functionality with one key difference: the execution of computer code. Thus, the Ethereum Project was born.

Ethereum blockchain lets developers create sophisticated programs that can communicate with one another on the blockchain.

Tokens

Ethereum programmers can create tokens to represent any kind of digital asset, track its ownership, and execute its functionality according to a set of programming instructions.

Tokens can be music files, contracts, concert tickets, or even a patient's medical records. Most recently, Non-Fungible Tokens (NFTs) have become all the rage. NFTs are unique blockchain-based tokens that store digital media (like video, music or art). Each NFT has the ability to verify authenticity, past history and sole ownership of the piece of digital media. NFTs have become wildly popular because they offer a new wave of digital creators the ability to buy and sell their creations while getting proper credit and a fair share of profits.

Newfound uses for blockchain have broadened the potential of the ledger technology to permeate other sectors like media, government, and identity security. Thousands of companies are currently researching and developing products and ecosystems that run entirely on burgeoning technology.

Blockchain is challenging the current status quo of innovation by letting companies experiment with groundbreaking technology like peer-to-peer energy distribution or decentralized forms for news media. Much like the definition of blockchain, the uses for the ledger system will only evolve as technology evolves.

Blockchain has a nearly endless amount of applications across almost every industry. The ledger technology can be applied to track fraud in finance, securely share patient medical records between healthcare professionals and even acts as a better way to track intellectual property in business and music rights for artists.

http://www.kavonichone.co.za/how-easy-is-it-doing-a-withdrawal-from-hyperfund/

https://scamwatcher.org/hyperfund-review/

https://filecoin.io/

https://hypergroup.io/overview/

https://makara.com/l/new?utm_campaign=12658159082&utm_source=google&utm_medium=cpc&utm_content=518742797029&utm_term=b_new%20crypto&adgroupid=123999688929&gclid=CjwKCAjw0qOIBhBhEiwAyvVcf879J01--azcTKr2CfmI1VOJIaHgu7a1sm9Dl4VnZ78CEQRt_MuAqBoCa0oQAvD_BwE

https://builtin.com/blockchain

https://www.hyperfund.com/

https://goallin.com.au/financial-freedom

https://www.investopedia.com/tech/most-important-cryptocurrencies-other-than-bitcoin/

https://www.investopedia.com/terms/h/hard-fork.asp